Primary vs Secondary Market: From IPO to the Stock Exchange

Here’s a question that trips up almost everyone who’s new to the market.

You open your app and buy ₹50,000 worth of shares in a big listed company. Where does your ₹50,000 go?

Most people assume it goes to the company. It doesn’t. The company doesn’t see a single rupee of it. Your money goes to some other investor you’ll never meet — someone who happened to be selling at that moment. The company isn’t even a party to the transaction.

That surprises people, and it should. Because it’s the entire difference between the primary market and the secondary market — and once you see it, a lot of things that seemed confusing suddenly aren’t.

The one-line version

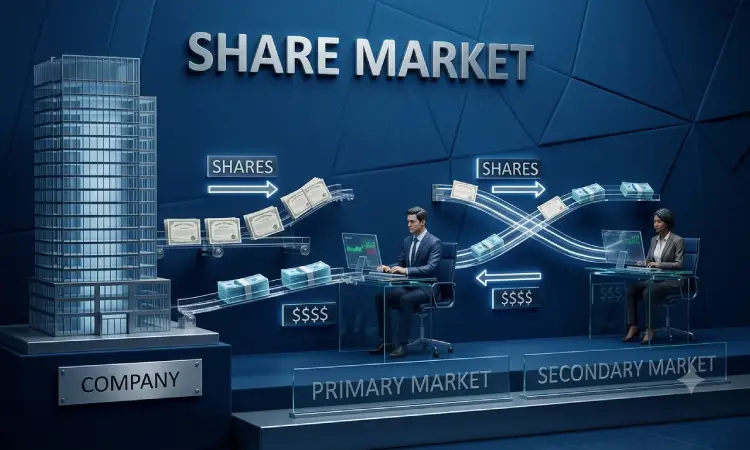

- Primary market: shares are created. Money flows from investors to the company.

- Secondary market: shares are traded. Money flows from investors to other investors.

A company raises money in the primary market once per issue. After that, its shares change hands in the secondary market forever, and the company is a spectator.

The IPO is the doorway between the two.

The primary market: where shares are born

The primary market is where securities come into existence for the first time. A company needs capital — for a factory, an acquisition, paying down debt — and instead of borrowing it, it sells ownership.

That’s the deal at the heart of every IPO. You give the company money. The company gives you a slice of itself.

The bit almost nobody explains: fresh issue vs offer for sale

Here’s where beginners get caught, and it matters more than any other detail on this page.

An Indian IPO usually has two components:

- Fresh Issue — brand-new shares created by the company. This money goes to the company. Genuine primary market.

- Offer for Sale (OFS) — existing shares being sold by promoters or early investors. This money goes to those selling shareholders. The company gets nothing.

Read a red herring prospectus and you’ll find the split stated plainly. Some IPOs are almost entirely OFS — which means the “company raising money” isn’t raising much at all. It’s early backers cashing out, using the IPO as an exit.

That’s not automatically sinister. Early investors are entitled to exit, and it’s disclosed. But an IPO that’s 90% OFS is a very different proposition from one that’s 90% fresh issue, and the offer document tells you which one you’re looking at. Most people never check.

The primary market isn’t only IPOs

An IPO is a company’s first public issue. Companies keep raising money afterwards:

| Route | What it is |

|---|---|

| FPO (Follow-on Public Offer) | An already-listed company issues more shares to the public |

| Rights Issue | New shares offered to existing shareholders first, usually at a discount |

| QIP (Qualified Institutions Placement) | A fast route to raise from institutions only |

| Preferential Allotment | Shares issued to selected investors |

| Private Placement | Sold to a small group, no public offer |

All primary market. All the same principle: new shares, money to the issuer.

From IPO to listing: the actual journey

Here’s how a company gets from “we want to go public” to “our stock is trading.”

1. The paperwork

The company files a DRHP (Draft Red Herring Prospectus) with SEBI — the document laying out its business, financials and, importantly, its risk factors. SEBI reviews it and issues observations. The company then files the RHP (Red Herring Prospectus) with the price band.

SEBI’s role here is worth being precise about, because it’s widely misunderstood: SEBI does not approve the price, and it does not vouch for the company. It checks that disclosure is adequate. Whether the price is sane is entirely your problem. (More on the regulator’s actual remit in our guide to what SEBI is and how it protects investors.)

2. Bidding opens

The issue stays open for a minimum of 3 working days (maximum 10). You apply through ASBA — Application Supported by Blocked Amount — which is a genuinely elegant piece of design:

Your money never leaves your account. It’s only blocked. If you get shares, it’s debited. If you don’t, the block simply lifts. There’s no “refund” in the old sense, because nothing was ever taken.

3. Who gets what

This is where most beginners have no idea what’s happening to them. For a standard book-built mainboard IPO — a company meeting SEBI’s profitability criteria under Regulation 6(1):

| Category | Quota | Who |

|---|---|---|

| QIB | Maximum 50% | Mutual funds, banks, insurers, FPIs (min 5% reserved for mutual funds) |

| NII / HNI | Minimum 15% | Applications above ₹2 lakh |

| Retail (RII) | Minimum 35% | Applications up to ₹2 lakh |

But if the company doesn’t meet those profitability norms — no average operating profit of at least ₹15 crore across the three preceding financial years — it can still list via the QIB route under Regulation 6(2). The maths flips hard:

| Category | Quota |

|---|---|

| QIB | Minimum 75% |

| NII | Maximum 15% |

| Retail | Maximum 10% |

And if QIBs don’t take up their 75%, the whole issue is cancelled and everyone’s money returns.

Understand what SEBI is telling you there. When a company hasn’t proven it can make money, the rules deliberately shrink the retail door and force professional institutions to underwrite the risk first. The allocation structure is a risk signal hiding in plain sight. If the retail quota is 10%, that’s not a quirk — it’s the regulator saying this one needs institutional scrutiny before your capital goes near it.

Anchor investors — a sub-category of QIBs, up to 60% of the QIB portion — commit before the issue opens. They can’t just flip: 50% of their allotment is locked for 30 days, the rest for 90 days.

4. The retail lottery — and the myth that costs people nothing but disappointment

If the retail book is oversubscribed, the registrar first tries to give every applicant at least one lot. When even that’s impossible, a computer draw decides.

Here’s the part worth tattooing somewhere: one PAN, one ticket. Applying for 13 lots instead of 1 does not improve your odds in the draw. And two applications on the same PAN don’t double your chances — they get all your bids rejected.

An IPO subscribed 50× in retail leaves roughly 49 of every 50 applicants with nothing. That’s not bad luck. That’s arithmetic.

5. T+3: from closing to listing

SEBI cut the listing timeline from T+6 to T+3, mandatory for issues opening on or after 1 December 2023. T is the issue closing date.

| Day | What happens |

|---|---|

| T | Issue closes |

| T+1 | Registrar finalises the basis of allotment |

| T+2 | Funds unblocked for unsuccessful applicants; shares credited to demat accounts |

| T+3 | Listing. Shares trade on the exchange |

Three working days from close to listed. That’s genuinely fast by global standards.

Listing day: the handover

This is the moment the primary market ends and the secondary market takes over.

On listing day the stock doesn’t just open at the issue price. It goes through a special pre-open session — order collection from 9:00 AM, then matching and a buffer — with normal trading beginning at 10:00 AM.

Sound familiar? It’s the same call-auction logic the whole market uses every morning: find the single price at which the maximum quantity can actually change hands. On listing day, that auction is doing something specific and dramatic — it’s the first time the market, rather than a merchant banker, gets to price this company.

If you want to understand what’s happening in that auction, it’s the same machinery we broke down in how stock prices are determined. The order book doesn’t care that it’s listing day.

And from 10:00 AM onwards, the company’s fundraising is finished. Forever, for that issue. Everything after this is investors trading with investors.

The secondary market: where shares actually live

99.9% of what you think of as “the stock market” is the secondary market. The NSE, the BSE, your app, the charts, the ticker.

Nothing new is created here. Shares that already exist simply move between owners. Your ₹50,000 goes to whoever sold. The company doesn’t participate and doesn’t benefit.

So why does the company care about its share price?

Fair question — if they don’t get the money, why does the CEO watch the stock?

Several real reasons:

- Future fundraising. A higher price means a future FPO or QIP raises more money for fewer shares. The secondary market sets the terms of the next primary raise.

- Collateral and credit. Share price affects the ability to borrow.

- Employee compensation. ESOPs are worth what the market says.

- Acquisitions. Buying a company with your own stock is cheaper when your stock is expensive.

- Careers. Boards and CEOs are judged on it.

So the secondary market disciplines the company continuously, without ever handing it a rupee. That’s the elegant part.

What the secondary market actually provides

Without it, the primary market would collapse. Ask yourself: would you hand a company money for a share certificate you could never sell?

Nobody would. Liquidity is what makes the primary market possible. The secondary market’s promise — you can leave whenever you want — is precisely what persuades investors to commit in the first place. The two markets aren’t rivals. One cannot exist without the other.

It also provides continuous price discovery, valuation for the whole economy, and a mechanism for savings to reach businesses.

The confusions worth clearing up

“Buying shares helps the company.” Only in the primary market. Buying on the exchange helps whoever sold to you.

“The IPO price is a fair price.” The IPO price is negotiated between the company and its bankers, with institutional demand shaping the book. It’s an asking price. Listing day is the first time the market votes on it — and the market frequently disagrees, in both directions.

“High grey market premium means a good investment.” The grey market is unofficial and unregulated. And there’s a counterintuitive trap: a hot GMP attracts a flood of applications, which reduces your odds of allotment. It tells you about sentiment, not value, and no regulator stands behind it.

“Oversubscription means the company is great.” It means demand exceeded supply at that price. Those are different claims.

FAQs

What is the main difference between the primary and secondary market? In the primary market, new shares are created and the money goes to the company issuing them. In the secondary market, existing shares are traded between investors and the company receives nothing.

Is an IPO part of the primary or secondary market? The primary market — it’s a company’s first sale of shares to the public. Once those shares list on the exchange, all further trading is secondary market.

Does the company get money when I buy its shares on the NSE? No. That money goes to the investor who sold you the shares. The company only receives money at the point of issue, in the primary market.

What happens between IPO closing and listing? Under SEBI’s T+3 timeline, allotment is finalised on T+1, funds are unblocked and shares credited on T+2, and listing happens on T+3 — where T is the issue closing date.

Does applying for more lots improve my IPO allotment chances? No. In an oversubscribed retail category, allotment runs on a computerised draw and it’s one PAN, one entry. Applying for more lots doesn’t add tickets. Multiple applications on the same PAN get all bids rejected.

Why is the retail quota only 10% in some IPOs? Because the company didn’t meet SEBI’s profitability criteria and listed via the QIB route, which requires at least 75% institutional allotment. It’s a deliberate limit on retail exposure to riskier issues.

Learn the market, not just the app

Understanding where shares come from — and why the money you spend on them doesn’t go where you assumed — is the kind of foundation that changes how you read everything else: an offer document, a listing pop, a rights issue announcement.

That’s what our stock market courses are built to give you. Not tips. Not calls. The actual machinery, taught in a classroom, from the ground up.

Dadar (Head Office): +91 99304 40999 | Thane: +91 99874 98599 Mon–Sat, 10 AM – 7 PM

Explore our courses · Admission process · Book free counselling